One factor that every small business owner should not overlook and treat as important as others is the wage and tax statement form, also known as the W-2 form. Each year by January 31, employers must send to employees these forms to file their income tax returns.

W-2 tax forms demand attention when filing. Failure to submit on time and improperly entered information could lead to fines. This article tackles everything you need to know when filing a W-2 form.

What is Form W-2?

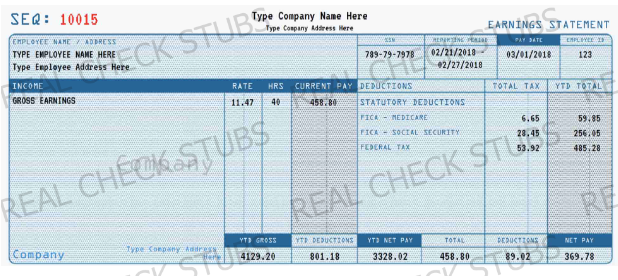

Form W-2, also known as the Wage and Tax Statement, is an Internal Revenue Service (IRS) tax form used by employers to report wages paid to their employees and the taxes withheld from them at the end of the year. As part of their responsibilities, employers must complete a Form W-2 for every employee in their company who receives a salary, wage, or other compensation.

The W-2 tax form includes salary and wage information for employees as well as withheld taxes such as federal, state, and other taxes. Employees use this information to complete their tax returns when filling up Form 1040.

The IRS requires employers to mail out the W-2 tax form on or before January 31. This allows taxpayers to prepare their tax returns before the income tax due date on April 15. This means an allowance of around two months for preparation.

The withholding amount entered into the W-2 form is deducted from a W-2 employee’s tax return for a tax year. The IRS could also issue refunds if an employer withholds more income than necessary.

Employers also use the wage and tax statement form to report FICA taxes to the Social Security Administration. Along with Form W-3, the employer files the W-2 form by the end of February with the Social Security Administration (SSA), which then reports to the IRS. The SSA uses the information on the form to calculate the Social Security benefits entitled to each worker.

The IRS also uses the tax form to monitor an employee’s tax liability. This makes it a formal proof of income for the SSA, court proceedings, and applications for federal financial aid for college.

Who Files Form W-2s?

As an employer who employs people in your business or company, you most likely would file the wage and tax form known commonly as the W-2 form. It is your responsibility to file and give each person receiving a salary, wage, or other compensation from you. However, this does not include independent contractors or self-employed workers, who need to use Form 1099 to report income statements.

According to the IRS, you need to give a W-2 form to any employee who earns more than $600, including non-cash payments. You would need to file the W-2 tax form before January 31 each year so that your employees have enough time to file their income taxes before the deadline.

To file for a wage and tax statement form, you would have to account for everything you paid to an employee, whether part-time, hourly, or salaried, or even if he or she worked for a short time. The form is still required even if the W-2 employee only worked for a day but earned $600 or more. The wage and tax form also requires you to account for any Medicare, Social Security, and taxes withheld from an employee’s paycheck.

Additionally, if you pay a family member working under your business or company and make $600 or more, you would need to submit a Form W-2.

Discover Legal Benefits Of W-2 Form For Both Employers & Employees

How To Complete The Lettered Boxes in W-2 Form?

When looking at a W-2 form, you would see both lettered and numbered boxes that you, as an employer, must fill out correctly and adequately.

Boxes A Through F

The lettered boxes on a wage and tax form include the employer and employee’s basic information.

A. Employee’s Social Security Number

B. Employer’s Identification Number (EIN)

C. Employer’s Legal Address

D. Control Number (if applicable/not required)

E. Employee’s Name appearing on their Social Security Number (SSN) card

F. Employee’s Address

Numbered Boxes 1 Through 10

- Box 1 shows the employee’s total taxable income, including salary, wages, tips, and bonuses in the tax form (if any).

- Box 2 details how much federal income tax is withheld from a W-2 employee’s paycheck.

- Box 3 shows the total earnings subject to Social Security Tax.

- Box 4 shows the total amount of Social Security tax the employer withholds for the year.

- Box 5 describes how much of the worker’s pay is subject to Medicare tax.

- Box 6 details the amount of Medicare tax withheld for the year.

- Box 7 shows the amount of tips a W-2 employee reports to their employer.

- Box 8 shows how much tip an employer allocated for their employee.

- Box 9 is for the 16-digit verification code needed to be entered when filing electronically. However, it reflects a now-defunct tax benefit, so not entering the code would not become a problem.

- Box 10 reports the total amount an employer pays to an employee towards dependent care benefits (if applicable).

Numbered Boxes 11 through 14

- Box 11 shows the amount of deferred compensation an employee receives from an employer through a Non-Qualified (Taxable) Deferred Compensation Program.

- Box 12 details all other types of compensation or reduction that have not been included but need to be included from an employee’s taxable income. Each amount corresponds to one of 31 different codes (A through FF), which include, for example, payments to a 401(k) plan.

- Box 13 of the tax statement form contains three sub boxes an employer chooses to report payments not subject to federal income tax withholding. The first option includes a statutory employee or independent contractor considered as an employee for tax withholding purposes. The second sub box shows if the employee participates in an employer-sponsored retirement plan. Lastly, the third option shows if an employee receives sick pay under an insurance policy.

- Box 14 has the same function as box 12, allowing an employer to report other tax-related information that might not fit into other sections of the W-2 tax form. This includes union dues and state disability insurance taxes, among others.

Numbered Boxes 15 Through 20

The last six boxes on the wage and tax form report information related to applicable state and local taxes. They include the amount of an employee’s pay subject to such taxes and the amount withheld from the paycheck.

- Box 15 shows an employer’s state tax ID number and the state where the business mainly operates.

- Box 16 details the amount of an employee’s taxable state wages.

- Box 17 shows how much state wages an employer already withheld for the year.

- Box 18 shows applicable local taxes.

- Box 19 details how much local tax an employer already withheld for the year.

- Box 20 provides the name of the locality where the employer withholds the taxes reported above.

Filing Requirements

As discussed earlier, employers need to complete and file the W-2 form and mail them to their employees by January 31 of each year. Employers filing the wage and tax form electronically to the Social Security Administration also have until the same deadline.

The form requires employers to make six copies:

Copy A – The employer completes this copy using red ink, making it the most distinct, and files it, along with W-3, to the Social Security Administration. Form W-3, which the employer must sign, summarizes all accomplished W-2 forms.

Copy B – Copy B reports federal income taxes, which the employer sends to the employee, who then files with their individual tax returns.

Copy C – The W-2 employee receives Copy C for purposes of record keeping.

Copy D – The employer retains Copy D for purposes of record keeping.

Copy 1 – Copy 1 goes to the applicable local governing body with the employer’s state or local income tax returns (if any).

Copy 2 – Copy 2 also goes to the applicable local governing body, but with the employee’s state or local income tax returns (if any).

The IRS requires employers to send W-2 tax form copies B, C, 1, and 2 to their employees by January 31 of the year, immediately succeeding the year which the W-2 form reflects. This gives W-2 employees approximately two months to prepare their income tax statement form due on April 15.

Along with W-3, the employer must file the wage and tax form with the Social Security Administration by the end of February.

Importance of Tax Withholding

As the employer, you withhold amounts from your employees’ paychecks for federal income taxes. Those amounts are then reported and remitted to the Internal Revenue Service (IRS) throughout the year using the W-2 form. The IRS requires everyone to file an income tax statement form and make periodic payments in a year.

For W-2 employees, when preparing federal returns and calculating the tax for the year, subtract from your tax bill the withheld amounts reported on the W-2 tax form. After doing so, you would know whether you would need to make an additional tax payment or receive a refund. This is also the case when filing state income returns. Perform the same calculations for the amount withheld to pay state income taxes.

Verifying Name and Social Security Number

The W-2 tax form’s identifying section essentially functions as a tracking feature. If the employee’s income reported on their taxes does not match the information provided in their W-2 form, the IRS would want to know why. The IRS would match the employer’s corporate tax return with the reported payment amounts to account for accuracy.

Additionally, since the IRS receives a copy of each employee’s wage and tax statement form, it knows whether an employee owes tax. The agency could also contact the W-2 employee if they fail to file for a tax return. The employer should check to see if the worker’s name and Social Security number are accurate.

Penalties for Late Filing of W-2 Form for Small Businesses

Late submissions of W-2 forms or wrong information reported means penalties for employers. That is why they need to file W-2s to the SSA and send them to their employees before the deadline.

The penalties could range depending on how late an employer submits the W-2 tax forms. If an employer fails to file a W-2 employee’s wage and tax form on time, the IRS could impose a penalty of $50 per W-2 if the employer files the correct form within 30 days of the deadline. The maximum penalty is $187,500 for small businesses. If the employer files between 31 days of the due date and August 1, the penalty increases to $110 per form with a maximum of $536,000.

Failure to file tax statement forms on or after August 1 incurs a fine of $270 per return or a maximum of $1,072,500 a year for small businesses. Lastly, intentionally neglecting to file comes with a $550 penalty per form with no limitation depending on the infraction.

The Internal Revenue Service considers a business a small business if it earns an average of $5 million or less in annual revenue for the past three tax years.

Extension for Filing W-2 Forms

Using the Application for Extension of Time to File Information Returns, also known as Form 8809, employers could ask for a 30-day extension for filing W-2 forms from the IRS. This gives employers a chance to catch up if they think they would miss the deadline. However, the IRS does not automatically grant extensions unless in “extraordinary circumstances or catastrophe.”

For example, suppose a business experienced a natural disaster such as a hurricane, tornado, or flood, or your records and books became a victim of fire. In that case, the employer could receive a favorable response on their extension request for filing the wage and tax statement forms.

Form 8809 should contain a detailed explanation of the reason for the extension, and the employer should sign it under penalty of perjury. The best time to file Form 8809 is between the 1st and 31st day of January or as early as possible.

Conclusion

Filing W-2 forms on time and correctly is an integral part of any small business. Take the time to create a check stub and have all essential information recorded properly each time you pay an employee. Understanding everything there is to know about W-2s would give you the advantage and eliminate problems in the future. A growing business comes with proper reporting of wage and tax statements.

Add Comment