Form 941 X: Instructions, Purpose, Complete, File

As an employer, accuracy in your tax filings is paramount. But what happens if you discover an error on your previously filed Form 941, the Employer's Quarterly Federal Tax Return?

That's where Form 941-X comes to the rescue. This comprehensive guide will walk you through everything you need to know about Form 941-X, ensuring you can confidently rectify any mistakes and remain compliant with IRS regulations.

In This Guide, You'll Learn:

- Purpose of Form 941-X: We'll delve into the specific situations where you need to file this form, from correcting wages and taxes to adjusting various credits.

- Form 941-X Instructions: We'll provide a detailed walkthrough of how to complete each section of Form 941-X, ensuring you understand the information required and the calculations involved.

- Filing and Deadline: You'll discover the proper procedures for submitting Form 941-X, including where to send it and the deadlines you need to adhere to.

- Common Mistakes to Avoid: We'll highlight common pitfalls that employers encounter when filing Form 941-X, helping you steer clear of potential issues.

- Tips and Best Practices: We'll share valuable insights to streamline the process and ensure a smooth filing experience.

What is Form 941-X?

Simply, Form 941-X serves for correcting a wide range of errors on Form 941. It, officially titled "Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund”.

Whether you underreported or overreported wages, taxes, or credits, this form allows you to make the necessary adjustments. It's your tool to ensure that your tax records accurately reflect your payroll and financial obligations.

Most people do not need to file a 941-X but there might be some years or quarters where you accidentally under or over report income and then you need to correct the mistakes so the IRS has the right information.

What is the purpose of Form 941-X?

Use Form 941-X to correct:

- Wages, tips, and other compensation;

- Federal income tax withheld from wages, tips, and other compensation;

- Taxable social security wages;

- Taxable social security tips;

- Taxable Medicare wages and tips;

- Taxable wages and tips subject to Additional Medicare Tax withholding;

- Qualified small business payroll tax credit for increasing research activities

Benefits of a 941-X Form

The main benefit of the 941-x form is that it allows you to correct mistakes without you needing to redo the original form. Rather than sending the original 941 back to you, the IRS allows you to use a different form to rectify the mistake.

You will send it back to the IRS when you are done so they can compare the two forms and then see that they have the right information.

Form 941-X Instructions

- You'll need a separate Form 941-X for each quarter with mistakes. These are generally filed separately from your regular Form 941, unless you didn't file a Form 941 previously due to misclassifying employees.

- If you never filed a Form 941, you'll need to file those instead of using Form 941-X, except if you misclassified workers and are now correcting that.

- When correcting errors, underreported tax credits are treated like overpayments, and overreported credits are treated like underpayments.

- Combine corrections for under- and over-reported amounts on one Form 941-X, unless you're claiming a refund. In that case, file separate forms for under- and over-reported amounts.

- The adjustment process is used for underpayments or when applying an overpayment credit to your current Form 941. The claim process is used for requesting refunds. A chart on page 6 of the form helps you choose the right process.

- Remember to explain each correction in detail on line 43 of Form 941-X. Also, continue reporting current quarter information (like tips and sick pay) on your regular Form 941.

- Additional steps are needed when filing Form 941-X, like certifying your W-2 filings. Don't use Form 941-X for other forms (like 943 or 945); instead, use their specific "X" forms.

How to Fill Out Form 941-X?

Explore the completing the 941-X form according to the latest revision of the form (April,2024)

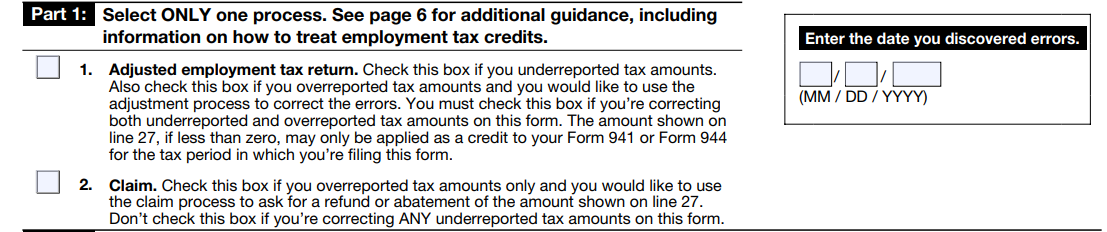

Part 1: Choose One Process

- Line 1 – Adjusted Return: Check this box if you're correcting underreported or overreported amounts and want to adjust the return. Any overpayment will be credited to your next Form 941 or 944.

- Line 2 – Claim: Check this box if you're only correcting overreported amounts and want a refund or abatement.

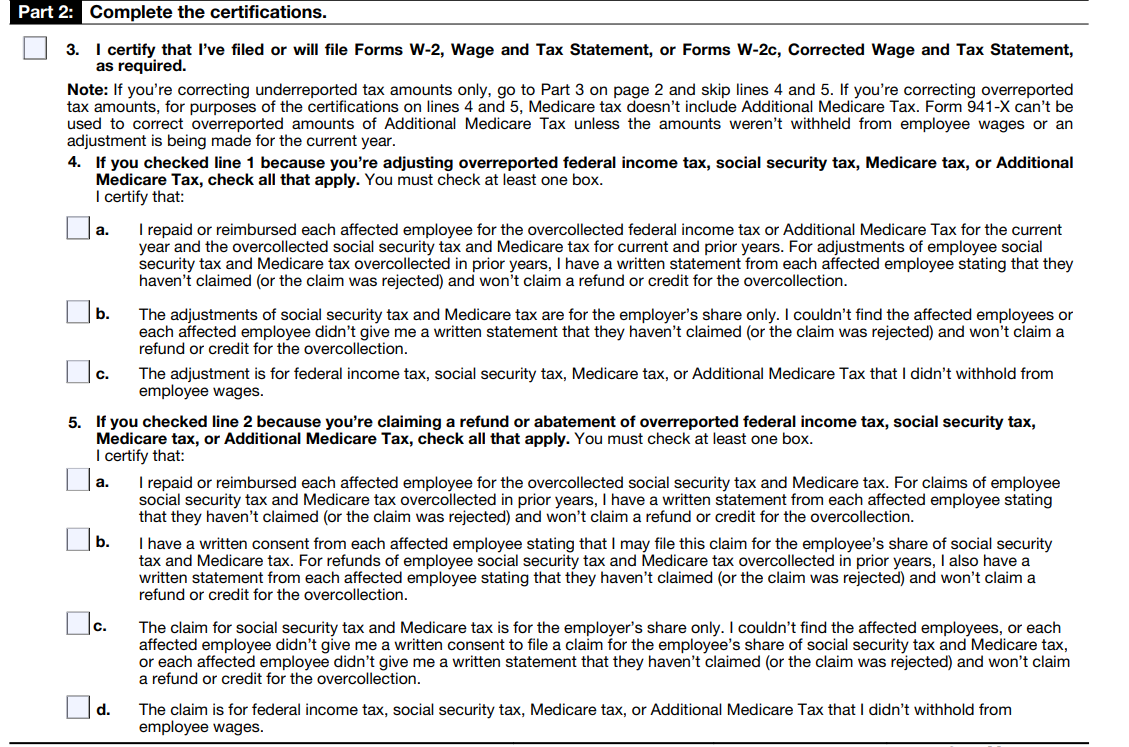

Part 2: Complete Certifications

- Line 3: Confirm you've filed or will file W-2s/W-2cs with the SSA.

- Lines 4 and 5: If you overreported taxes, certify how you'll handle employee refunds or obtain their consent to file a claim on their behalf.

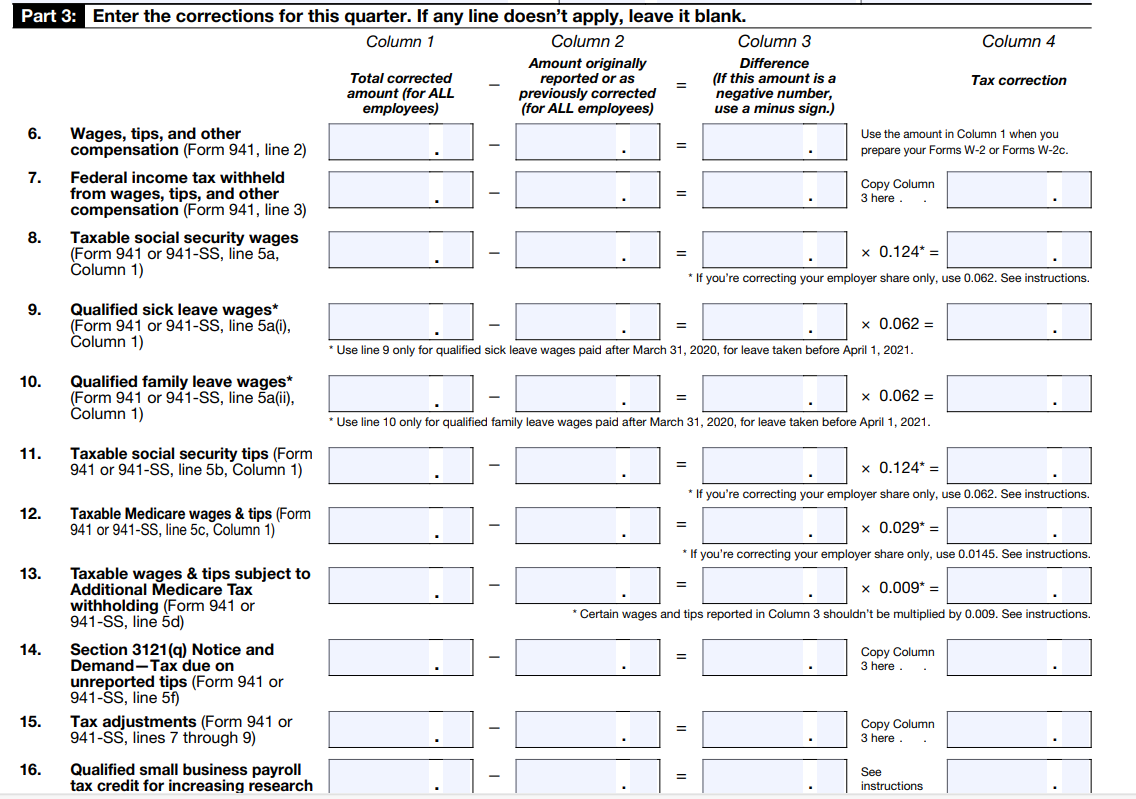

Part 3: Enter Corrections

- Lines 6-13: Report corrected amounts for wages, tips, and taxes for ALL employees.

- Lines 14-22, 25-26c, 28-32, 35-40: Special instructions apply, read carefully.

- Line 27 – Total: Calculate the total difference from corrections. Negative means you overpaid, positive means you owe.

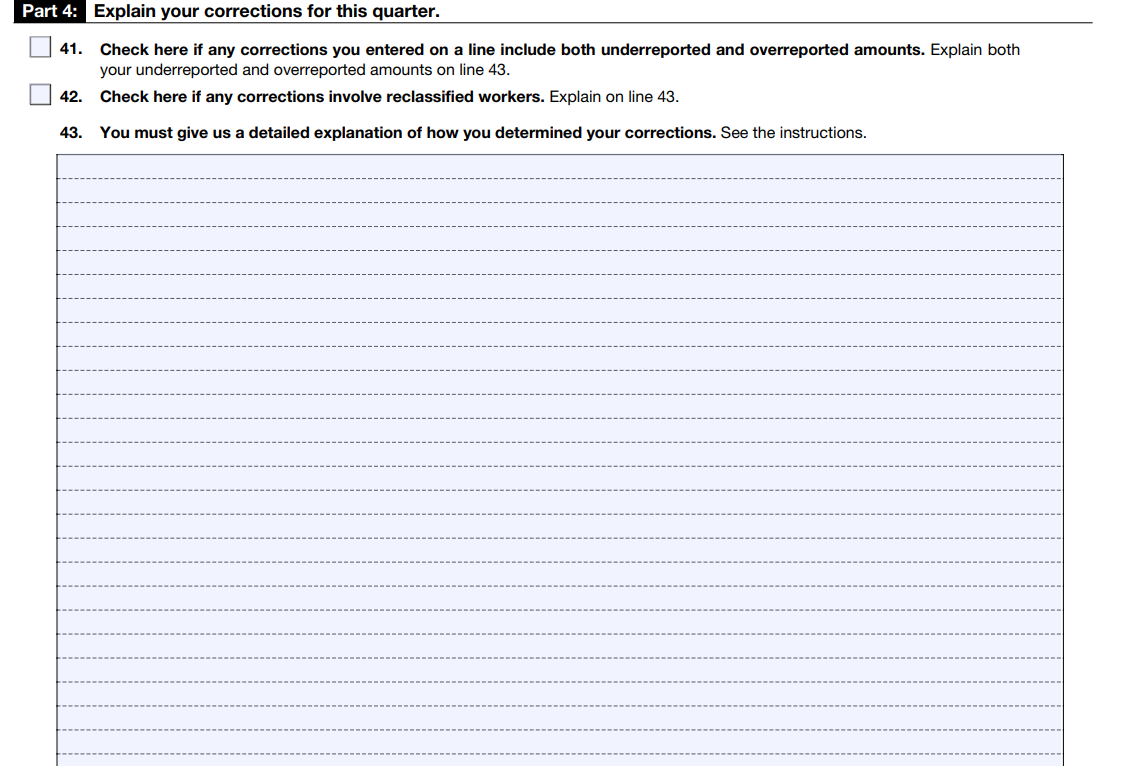

Part 4: Explain Corrections

- Line 41: Check if corrections include both under- and over-reported amounts.

- Line 42: Check if any workers were reclassified.

- Line 43: Provide a detailed explanation for each correction, including amounts, dates, and causes.

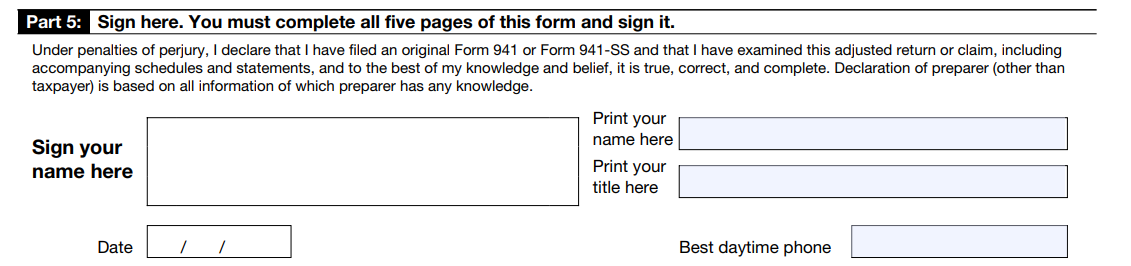

Part 5: Sign the Form

The form must be signed by an authorized person (owner, officer, partner, etc.) or their agent with a valid power of attorney.

Paid Preparer Use Only

If you're a paid preparer who isn't an employee of the company filing Form 941-X, you must sign the form and fill out the "Paid Preparer Use Only" section. This includes your PTIN, full address, and your firm's name and EIN if applicable. You must also provide a copy of the form to the taxpayer.

Reporting agents generally don't need to complete this section, unless they offered legal advice on matters like worker classification.

When to File Form 941-X?

File Form 941-X upon discovering an error on a previously filed Form 941, except for errors related to the number of employees or federal tax liabilities (those are corrected elsewhere).

Due Dates:

- Underreported Tax: File by the due date of the return for the period when you found the error, and pay any owed amount by then. This usually avoids interest and penalties.

- Overreported Tax - Adjustment: File as soon as possible, but more than 90 days before the period of limitations expires.

- Overreported Tax - Claim: File anytime before the period of limitations expires.

Specific Due Dates for Underreported Tax:

|

Quarter with Error |

Form 941-X Due |

|

Q1 (Jan-Mar) |

April 30 |

|

Q2 (Apr-Jun) |

July 31 |

|

Q3 (Jul-Sep) |

October 31 |

|

Q4 (Oct-Dec) |

January 31 |

Is There a Deadline for Filing Form 941-X?

- Overreported Taxes: Generally, within 3 years of filing the Form 941 or 2 years from the payment date, whichever is later.

- Underreported Taxes: Within 3 years of filing the Form 941.

Note: If filing in the last 90 days of the period of limitations for overreported taxes, you must use the claim process.

Example:

If you overpaid taxes on your Q2 2023 Form 941 filed on July 31, 2023, and discovered the error on June 15, 2026, you must file Form 941-X using the claim process by July 31, 2026.

Where Should You File Form 941-X?

If you can, submit your Form 941-X online (IRS encourages you to file Form 941-X electronically). If you choose to mail a paper Form 941-X, send your completed Form 941-X to the address below:

Form 941-X Mailing Address

|

IF you’re in . . . |

Then mail form 941-X to this address : |

|

Connecticut, Delaware, District of Columbia, Florida, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin |

Department of the Treasury Internal Revenue Service Cincinnati, OH 45999-0005 |

|

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming |

Department of the Treasury Internal Revenue Service Ogden, UT 84201-0005 |

|

No legal residence or principal place of business in any state |

Internal Revenue Service P.O. Box 409101 Ogden, UT 84409 |

|

Special filing address for exempt organizations; federal, state, and local governmental entities; and Indian tribal governmental entities, regardless of location |

Department of the Treasury Internal Revenue Service Ogden, UT 84201-0005 |

Important Warnings and Penalties

⚠️ Critical Notice: Failure to file Form 941-X by the required deadline may result in penalties and interest charges on any underpaid amounts. For complex corrections involving multiple quarters, worker reclassification, or significant dollar amounts, consult a qualified tax professional or CPA. Filing Form 941-X may increase the likelihood of IRS review of your payroll records.

Common Error Examples That Require Form 941-X

Understanding specific scenarios helps identify when you need to file Form 941-X:

- Wage Misclassification Example: If you discover that a contractor should have been classified as an employee, requiring Social Security and Medicare tax withholding.

- Calculation Error Example: Incorrectly calculating overtime wages that resulted in underreported regular and overtime compensation.

- Credit Overclaim Example: Claiming more Employee Retention Credit than allowable, requiring correction and potential repayment.

- Tip Reporting Error: Restaurant failing to properly report employee tip income, leading to underreported wages and taxes.

Electronic Filing Options and Requirements

While the IRS encourages electronic filing, here are the specifics:

- E-file Requirements: Electronic filing requires IRS-approved software and a valid Electronic Filing Identification Number (EFIN).

- Approved Software: Popular e-filing options include major tax software providers or work with a tax professional who offers electronic filing.

- Processing Times: Electronic submissions typically process faster than paper returns, with confirmation receipts provided immediately.

- System Limitations: Note that some complex corrections may still require paper filing depending on the software capabilities.

Required Documentation and Record Keeping

Documentation Checklist:

- Copies of original Form 941 being corrected

- Corrected W-2 forms (if applicable)

- Payroll records supporting the corrections

- Bank records showing tax deposits

- Documentation of worker reclassification (if applicable)

Record Retention: Maintain all supporting documentation for at least 4 years from the date the tax became due or was paid, whichever is later.

Submission Guidelines: Do not submit supporting documents unless specifically requested by the IRS, but have them readily available for review.

Common Filing Mistakes to Avoid

- Filing separate 941-X forms when one combined form would suffice

- Incorrectly calculating the net difference in Part 3

- Failing to update employee W-2 forms when required

- Missing the 90-day rule for claim vs. adjustment process

State Tax Implications

Remember to check if your state requires similar corrections to state payroll tax returns. Contact your state tax agency to determine if additional forms are needed.

What to Expect After Filing

Once you submit your Form 941-X, typical IRS processing timeframes vary by filing method, with electronic submissions generally processed faster than paper forms. Refunds or credit applications are processed according to IRS schedules, which can range from several weeks to several months depending on the complexity of your correction and current processing volumes.

You can track submission status through IRS online tools or by calling their business tax line for updates on your filing. Respond promptly to any IRS correspondence regarding your filing, as delayed responses may result in additional processing time or potential penalties.

Allen Wood is an accomplished accountant with over 15 years of experience in the field.

Our all Posts