How To Estimate Adjusted Gross Income From Pay Stub?

Tax Day, the day our income tax returns are due, isn’t a day most Americans look forward to. It rolls around each year, typically on April 15th, and still catches people off-guard who feel like they just submitted their previous income tax return.

If you fall into this camp, it’s not surprising, considering how complicated tax returns have gotten even for the average taxpayer.

However, if a taxpayer’s main source of income comes from a regular job, they can often estimate their adjusted gross income (AGI) by using their last pay stub for the tax year.

This article explains how to estimate AGI using your pay stub and reviews the latest IRS rules, income limits, and deductions that can affect your calculation.

What is Adjustable Gross Income?

Adjustable gross income is a taxpayer's total taxable income before the federal government's allowable deductions and includes all income earned in addition to what was reported on the W-2. Other forms of income added to calculate adjusted gross income can include dividends, pensions, capital gains, etc.

Your AGI appears on line 11 of Form 1040 (U.S. Individual Income Tax Return)

2025 Note: The IRS inflation adjustments have slightly raised deduction limits and income thresholds across all tax brackets. For 2025, the standard deduction is:

$14,600 for single filers

$29,200 for married filing jointly

$21,900 for heads of household

(IRS Revenue Procedure 2024-55, released Oct 2024)

Above-the-Line vs. Below-the-Line Deductions

"Above-the-line" and "below-the-line" refer to the two main types of tax deductions.

Above-the-line deductions are the first ones you can claim. These are things like 401(k) contributions and student loan interest. Most people can use these deductions, and when you take them out of your gross income, you get your adjusted gross income.

Once you reach your adjusted gross income, you can claim the standard deduction, a fixed amount that depends on your filing status (single, married filing jointly, married filing separately, head of household, or qualifying widow(er)).

Some people may be able to claim below-the-line deductions, which are also called itemized deductions. This happens more often in high-income households with a lot of qualifying expenses, like giving to charity and paying a lot of interest on their mort

⚖️ Most taxpayers still save more by taking the standard deduction rather than itemizing. However, the 2025 “One Big Beautiful Bill” (OBBB) raised the SALT deduction cap to $40,000 for married couples, which may make itemizing worthwhile for some high-income households.

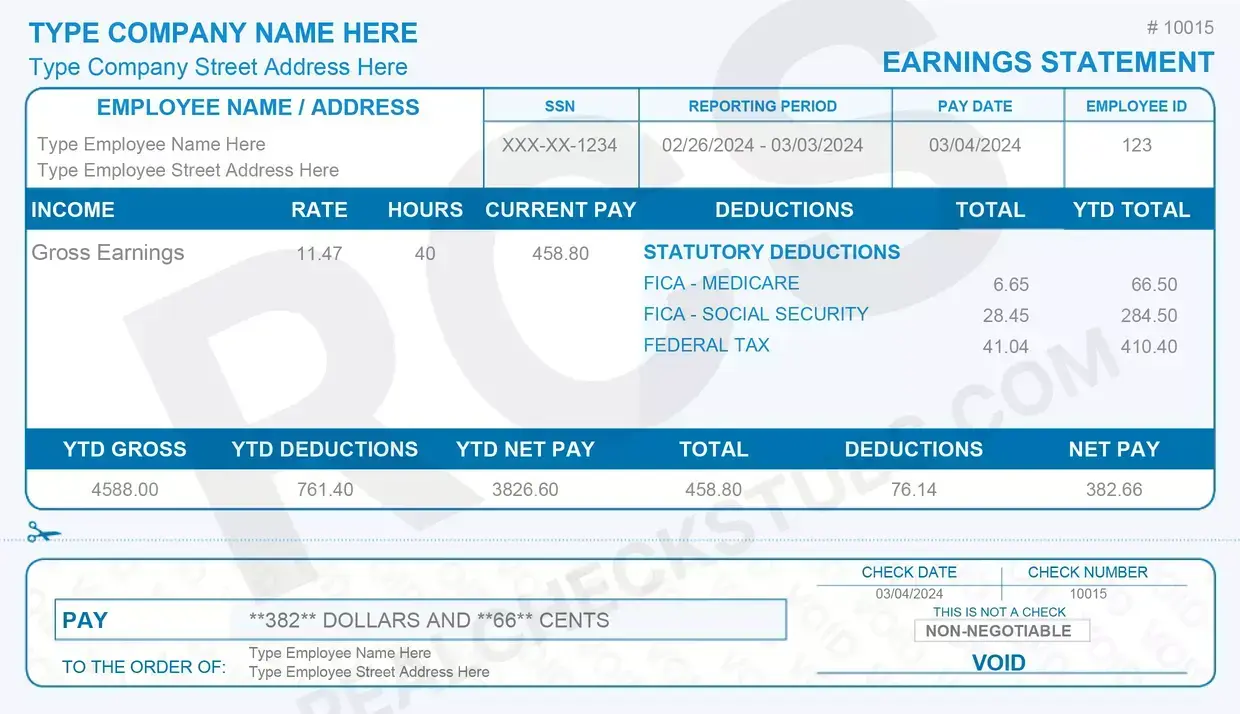

What Information Does a Pay Stub Include

Even though each state may have specific rules on the information a pay stub must include, the important pieces of information are typically the same for states requiring employers to give their employees pay stubs. Listed below are typically the main earnings and deductions components found on a pay stub.

Gross Pay

Gross pay, also known as gross earnings or gross wage, is an employee's total pay for that period. This can be derived by multiplying the hourly wage by hours worked or by dividing an annual salary by the number of pay periods. There will also be gross pay year-to-date (YTD), which is simply the gross income earned to date. Gross pay may also be broken down into its components, such as commission, vacation pay, etc.

Federal Income Tax

Employers are required to withhold federal income taxes from their employee's paychecks and remit the taxes withheld to the Internal Revenue Service (IRS) of the Federal Government. Paystubs will typically have the federal income tax deducted for the pay period on the pay stub, as well as the YTD total.

State Income Taxes

Employers must withhold state income taxes from their employee's paychecks and remit them to their respective states. Paystubs will typically have the state income tax deducted for the pay period of the pay stub and the YTD total. There are nine states where employees do not pay income tax to their state governments, and these include Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

Federal Insurance Contribution Act Taxes

The Federal Insurance Contribution Act (FICA) includes Medicare and Social Security statutory federal tax contributions. Employers are required to withhold these payroll taxes for each pay period and remit them to the IRS of the Federal Government.

Net Pay

Net pay is the amount of cash the employer pays their employee after they have withheld the required federal taxes, state taxes, Medicare, and Social Security federal payroll taxes. It is important to note that in addition to withholding taxes, it is also common to have other deductions on a pay stub for the pay period, such as for retirement and insurance that reduce net pay, also known as net income.

If you don’t have a recent pay stub, you can easily create one for reference using our pay stub generator!

Estimating Adjusted Gross Income from a Pay Stub

You can estimate your AGI from your final pay stub of the year, especially if you only have one job.

If you have multiple income sources, additional income, or deductions, your AGI calculation will require more details.

But you can calculate your AGI from W2 Form.

Adjustments to Taxable Income

Taxpayers are required to pay tax on additional income earned through the tax year in addition to YTD gross pay noted on their pay stub; however, they will also be able to reduce their income with allowable deductions. The information below includes a brief explanation of additions and subtractions to determine adjusted gross income, followed by three adjusted gross income calculation examples.

Additions to Income

Taxpayers must pay tax on other income earned in the tax year in addition to their main source of income, such as unemployment compensation, alimony, dividends, and so on. This income will be added and then summed on line 9 of Schedule 1 of Form 1040.

Subtractions to Income

Taxpayers can reduce their gross income with allowable adjustments that include, in part, educator expenses, moving expenses, paid alimony, student loan interest, etc. All permissible adjustments to income will be summed and reported on line 26 of Schedule 1 of Form 1040.

AGI Calculation Example #1

John Smith is 25 years old and only has one source of income. His last pay stub of the year noted a gross income of $45,000 YTD. John only has one source of income and does not qualify for the allowable deductions such as educator or moving expenses. To calculate his adjusted gross income, we only need to use his reported gross pay noted on his last pay stub of the year.

Adjusted Gross Income = $45,000

AGI Calculation Example #2

Peter Smith is a 30-year-old school teacher, and his last pay stub of the year notes his gross pay of $35,000, which matches the annual salary in his employment contract. John also works a part-time job to help pay off the student loan required to become a teacher. John will use his last pay stub of the year from his teaching job and a part-time job to determine his total income. He will then determine the amount of interest he paid on his student loans for the year and then calculate his adjusted gross income.

- Teaching Pay Stub YTD Gross Pay = $35,000

- Part-time Job Pay Stub YTD Gross Pay = $6,000

- Total Income = $41,000

- Interest Paid on Student Loan = ($1,500)

- Maximum Educator Expense Deduction = ($300)

- Total Deductions = ($1,850)

- Total Income = $41,000

- Total Deductions = ($1,800)

Adjusted Gross Income = $39,200

AGI Calculation Example #3

Sarah Smith is 45 years old, has one primary source of income, and also receives alimony from her ex-husband. Her annual salary is $55,000, is paid bi-monthly, and her last pay stub of the year shows a gross income equaling her annual salary of $55,000. Sarah’s yearly alimony income is $12,000.

- Pay Stub YTD Gross Pay = $55,000

- Annual Alimony Payments = $12,000

Adjusted Gross Income = $67,000

NOTE: Alimony received is ONLY taxable if your divorce was finalized BEFORE January 1, 2019.

- Pre-2019 divorces: Alimony IS taxable income (add to AGI)

- 2019+ divorces: Alimony is NOT taxable income (don't add to AGI)

This change is permanent under the Tax Cuts and Jobs Act (TCJA).*

Source: IRS Topic No. 452, "Alimony and Separate Maintenance"

(www.irs.gov/taxtopics/tc452)

Can You Find Adjusted Gross Income on Your Pay Stub?

No — your pay stub doesn’t directly show your Adjusted Gross Income (AGI). However, you can estimate it using information already listed on your final pay stub of the year.

Can You Find Adjusted Gross Income on Your W-2?

No, the W-2 does not list AGI. AGI is calculated on Form 1040, line 11, incorporating your W-2 amounts plus any additional income and adjustments.

If you are paid, your employer will complete a W-2 form to record your earnings and mail it to you. Box 1 shows the entire amount of "wages, tips, and other remuneration" you received. However, keep in mind that this is not your adjusted gross income.

The total amount of your taxable income from that employment may be seen in Box 1 of your W-2 form. It excludes various above-the-line deductions that are part of calculating your adjusted gross income. For example, your total "wages, tips, and other remuneration" does not include funds paid for health savings account contributions or student loan interest.

Need to Know: Are Tips Taxable?

If you work part-time for more than one company or switch employment during the year, you will receive multiple W-2 forms (one for each employer). You may also have income from sources other than your W-2, such as renting a property you own.

When tax season comes around, you’ll receive your official Form W-2 from your employer — or you can easily create one yourself using our W-2 form maker!

Non-Yearend Pay Stub

If you want to estimate your AGI before the year ends, multiply your YTD income by the number of remaining pay periods to project your total annual income. You can calculate an estimated adjusted gross income from any pay stub, but it won't be the final number until the fiscal year has ended.

For example, a taxpayer has a yearly salary paid over 24 pay periods per year. To calculate the estimated adjusted gross income for the year, they can simply take the YTD gross income on their pay stub and add anticipated income from the remaining pay periods.

How to Find AGI if You E-File?

Remember that you may receive and utilize an IP-PIN (Identity Protection - Personal Identification Number) instead of your 2023 AGI during the tax return e-Filing procedure.

Here are three reliable ways to locate your Adjusted Gross Income (AGI):

1. Check your most recent tax return.

If you filed your tax return online (for example, through eFile.com or another e-file service), sign in to your account and download the PDF copy of your latest return.

→ Your AGI appears on Line 11 of Form 1040, Form 1040-SR, or Form 1040-NR.

2. Use a paper or saved digital copy.

If you filed elsewhere or kept your return from a previous year, open your saved copy and look for Line 11 on Form 1040 — that line always shows your AGI, regardless of tax year.

3. Request a free IRS transcript.

If you no longer have a copy of your return, you can request a free transcript directly from the IRS at

👉 https://www.irs.gov/individuals/get-transcript

.

The transcript will list your “Adjusted Gross Income” exactly as it appears on your filed tax return.

Note: This is a free service given by the IRS, and your previous year's AGI will be reflected as ADJUSTED GROSS INCOME on the transcript.

2025 Highlights to Note

- SALT deduction cap raised to $40,000 (for joint filers)

- No federal tax on tips up to $25,000 for eligible workers

- Senior Bonus Deduction added for taxpayers aged 65+ under certain AGI limits

- Increased Social Security wage base ($176,400)

- Standard deduction and tax bracket thresholds adjusted for inflation

Summary

You can estimate your Adjusted Gross Income (AGI) from your pay stub by reviewing:

- Your YTD gross pay,

- Adding any additional income,

- Subtracting allowable adjustments and deductions.

For most people with one job, this provides a solid estimate — but for more complex income (investments, self-employment, etc.), you’ll need your Form W-2 and Form 1040 to calculate accurately.

References:

Allen Wood is an accomplished accountant with over 15 years of experience in the field.