Why Was No Federal Income Tax Withheld From My Paycheck?

Quick answer: don't panic. That $0 may be correct. Before anything else, look at two things. First, your gross pay. For a single filer with a standard 2026 W-4, federal withholding doesn't even start until roughly $310 a week, which works out to about $16,100 a year, the 2026 standard deduction. Below that, zero withheld is the system working. Second, your W-4. Did you claim exempt? Enter dependents? Pretty much everything happening on your paycheck traces back to that form, so pull up a copy if you can. This article shows you exactly what to look for.

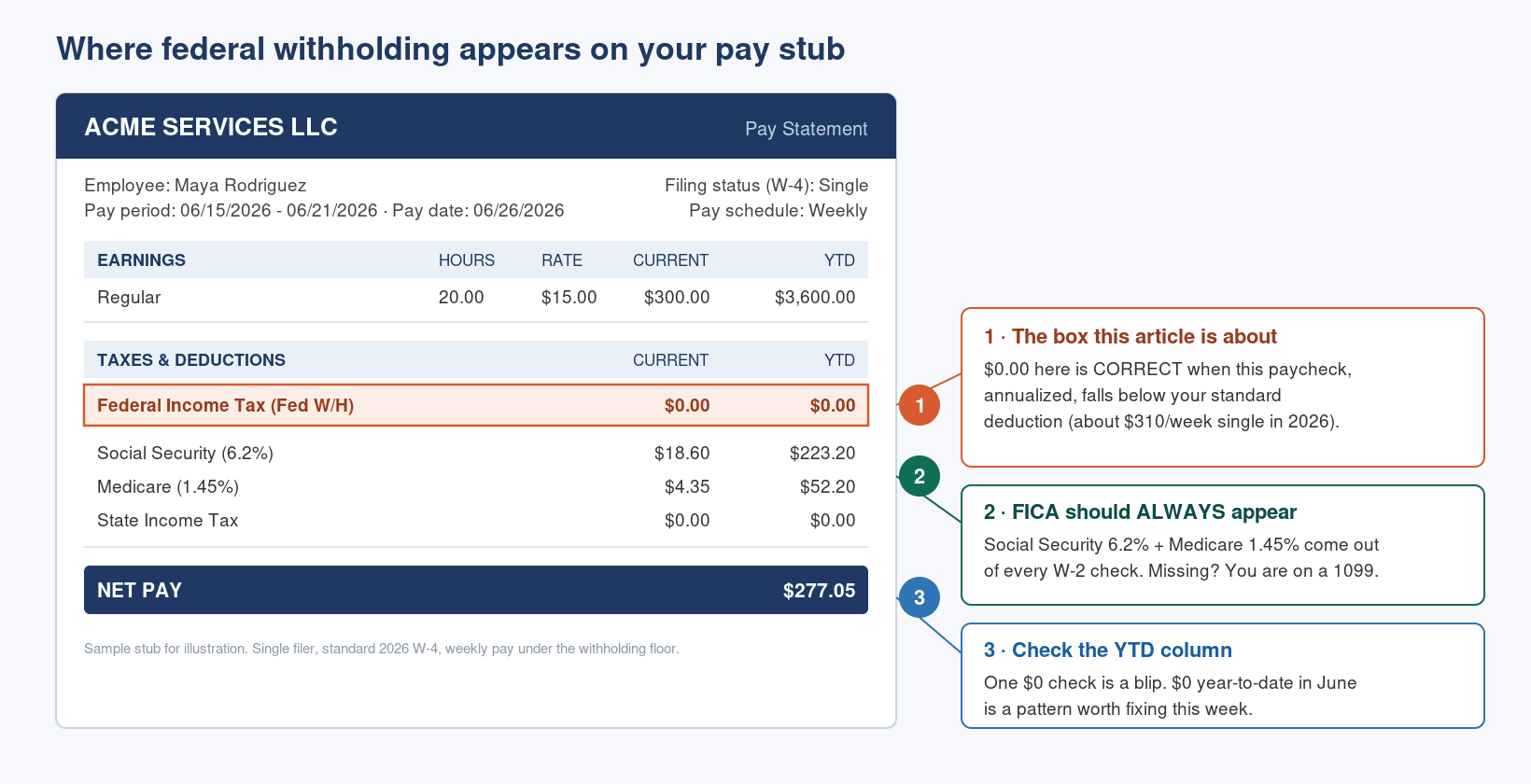

(One quick check while you have the stub out: Social Security (6.2%) and Medicare (1.45%) should still be coming out of every check. If those are missing too, jump to reason #4. You may be paid as a contractor.)

First: is $0 actually wrong?

Not necessarily. Withholding is designed to match the tax you'll actually owe for the year. If your yearly income lands below the 2026 standard deduction ($16,100 single, $32,200 married filing jointly, $24,150 head of household), your income tax bill is $0, so there's nothing for your employer to withhold.

That's why a part-time paycheck often shows zero while a full-time coworker's shows a deduction. Their bigger check triggers withholding; yours doesn't. Same rules, different numbers.

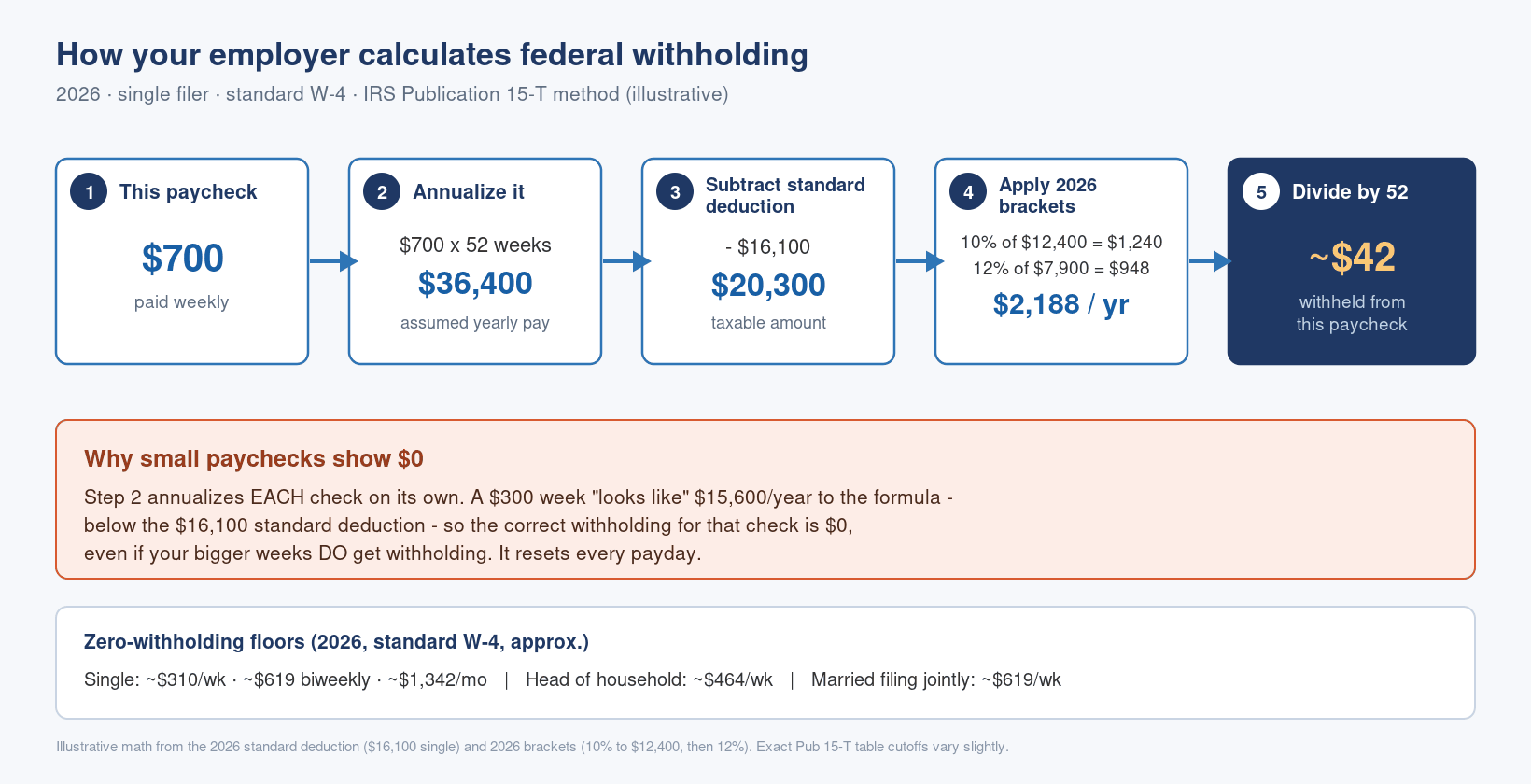

How your employer actually figures it (the annualizing trick)

Here's the nuance most people never hear: your withholding is based on an annualized number, not your actual yearly income. Your employer doesn't know you'll make $32,000 this year. They make their best guess one paycheck at a time.

Say you're paid weekly. They take this week's check and multiply by 52. Make $700 this week? The system treats you like a $36,400-a-year earner and withholds accordingly, about $42 on that check. Make $300 next week? Now it treats you like a $15,600 earner. That's below the $16,100 standard deduction, so that check gets zero. Every check is treated this way, independently.

Two things follow from that:

- If your hours swing, your withholding swings. Small shifts, big shifts: the withholding will look all over the place, and that's normal. But the more your pay varies, the more your actual year-end result can drift from what got withheld, in either direction.

- Two part-time jobs is the classic trap. Each job only sees its own paychecks. If neither one crosses the threshold by itself, both withhold $0 while your combined income is very much taxable. (The fix is in the W-4 section below.)

The 2026 zero-withholding thresholds

Approximate pay levels below which a standard W-4 produces no federal withholding. (Method validated against the IRS's own 2026 Pub 15-T example; exact wage-bracket rows round within a few dollars.)

| Pay schedule | Single / MFS | Head of household | Married filing jointly |

|---|---|---|---|

| Weekly | ~$310 | ~$464 | ~$619 |

| Biweekly | ~$619 | ~$929 | ~$1,238 |

| Semimonthly | ~$671 | ~$1,006 | ~$1,342 |

| Monthly | ~$1,342 | ~$2,013 | ~$2,683 |

The 6 reasons, ranked

1. Your pay is too low

Covered above. The most common reason, and usually fine. Includes the two-part-time-jobs trap.

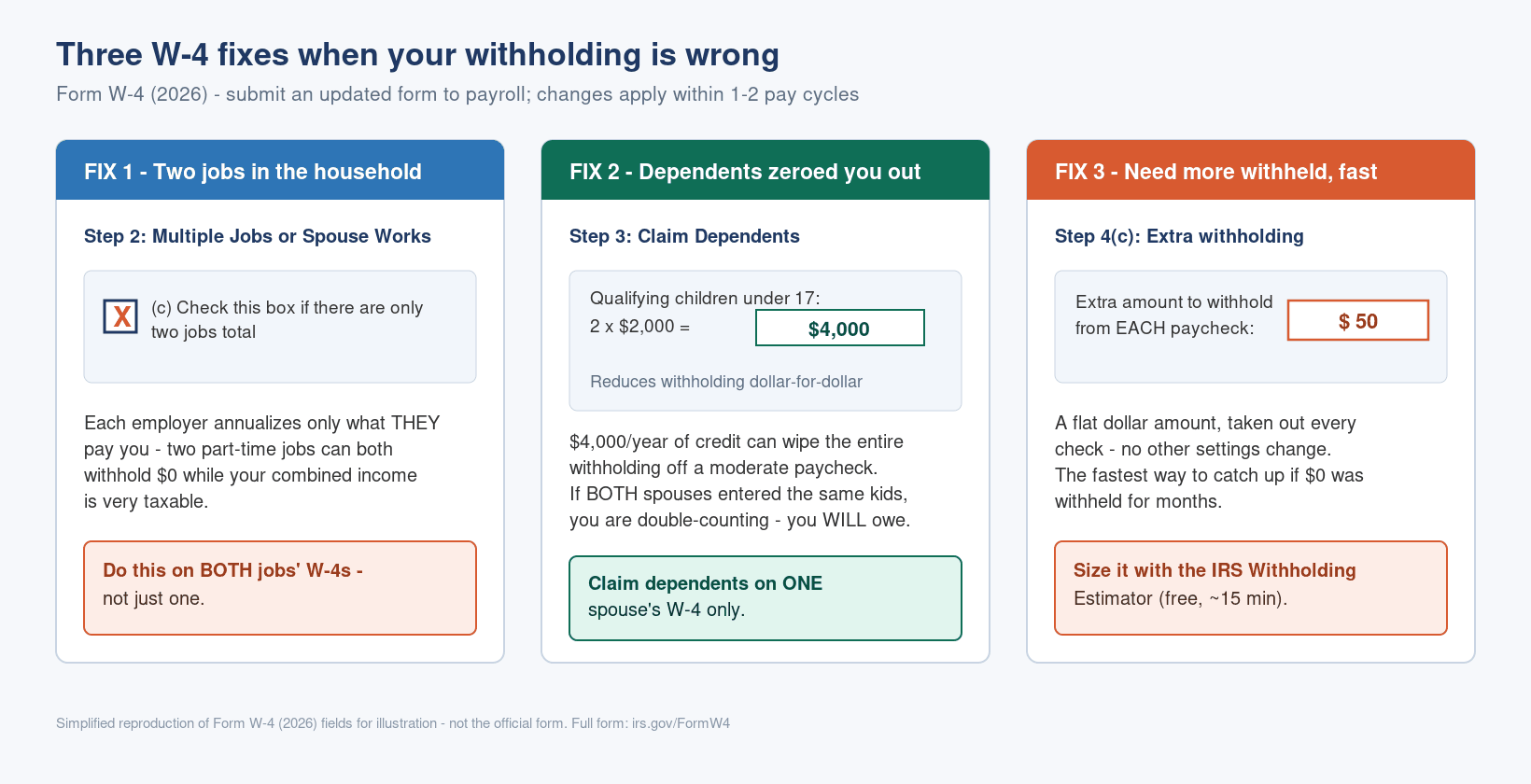

2. The dependents you claimed on your W-4

Every $2,000 of child tax credit entered in Step 3 reduces your withholding dollar-for-dollar across the year, which is enough to zero out a moderate paycheck. The trap for couples is double-dipping: if both spouses enter the same two kids on both W-4s, the same credit gets counted twice and you'll owe. Never claim the same child on two W-4s. Have one spouse claim them, or split them one each, so the withholding reflects reality.

3. You claimed exempt

Here's one we see constantly. We once reviewed a pay stub with zero withholding that clearly shouldn't have been zero. Went back to her W-4, and there it was: an exemption marked. Someone had told her that's how they handled their own withholding, and it sounded like a good idea, so she did the same. That's the problem with exempt. It has conditions (you owed zero tax last year AND expect zero this year), and if you don't actually meet them, you're not avoiding tax. You're deferring it to April, sometimes painfully.

A payroll detail worth knowing: exempt status expires every February 15 (IRS Topic 753). To stay exempt you must file a fresh W-4 by that date each year. Miss it, and your employer is required to start withholding as if you're single with no adjustments. How strictly that reset gets applied varies by payroll provider, so people go from $0 withheld to suddenly seeing withholding (or keep an exempt status they no longer qualify for) without anyone telling them. And there are no do-overs: taxes withheld while your exempt claim lapsed don't get refunded by payroll. If you don't remember claiming exempt, ask what's on file.

4. You're a contractor (1099)

No W-4, no withholding at all. No federal income tax, and no FICA lines on your pay statement either. You're responsible for quarterly estimated payments (Form 1040-ES), including roughly 15.3% self-employment tax. If your "employer" sets your hours and directs your work but pays you on a 1099, look into misclassification (IRS Form SS-8).

5. Cross-state complications

Working across state lines gets wacky: reciprocity agreements, nonresident certificates, states with no income tax at all. Those mostly hit the state line, but multi-state setups are where payroll systems get misconfigured and the federal side catches a stray. If you moved, or you work in a different state than you live, have payroll re-verify your setup.

6. Employer error

It happens: a W-4 keyed in wrong, the wrong box clicked, a form uploaded incorrectly. That's a compliance issue on their end, but the tax liability is still yours. This is exactly why you should keep a copy of every W-4 you submit. When the stub looks wrong, you can compare against what you actually filed instead of arguing from memory.

No, there is no "$600 rule" for withholding

You may have read (including, previously, on this site) that employers don't withhold federal income tax on paychecks under $600. That's not true, and we're correcting the record. No dollar-amount rule exempts small paychecks from withholding. It's the annualizing math above, nothing else. The $600 figure comes from a different rule entirely: the long-standing threshold for issuing a Form 1099 to a contractor. That's a reporting rule, and it has nothing to do with paycheck withholding. (That threshold rises from $600 to $2,000 for payments made starting January 1, 2026, under OBBBA, and adjusts for inflation after that. Which means the "$600 rule" people keep repeating isn't even the right number for its own rule anymore.)

Check your own stub (60 seconds)

Quick vocabulary first, because these get mixed up. FICA is Social Security (6.2%) plus Medicare (1.45%). Those come out of every W-2 paycheck, always. Federal Income Tax (often "Fed W/H" or "FIT") is the separate line this article is about, the one that can legitimately be $0.

- Find the Federal Income Tax / Fed W/H line, current and YTD.

- Confirm the FICA lines exist (6.2% + 1.45%). Missing entirely means you're on a 1099.

- Check the YTD column. One $0 check is a blip; $0 year-to-date in June is a pattern. Act this week.

- Compare your gross against the threshold table for your filing status.

Want to see how these boxes work with your own numbers? Our pay stub generator calculates federal, state, and FICA lines exactly as they appear on a real stub.

How to fix it

A note from the payroll side first: payroll isn't permitted to tell you what to put on your W-4. Employers can explain the form and the deadlines, but they're not allowed to give tax advice on what you should claim. And honestly, that protects you. The W-4 exists to personalize your withholding; there are no blanket rules. Your coworker's W-4 reflects their kids, their spouse's job, their hours. People think they can look at someone else's paper and copy it down, and that's how you end up in a worse spot than if you'd just answered the form honestly. The form is frustrating and the jargon is real, but it's your numbers or nothing.

So instead of guessing:

- Run the IRS Tax Withholding Estimator (free, about 15 minutes). It gives you clarity on exactly what your W-4 should say for your situation.

- Submit a new W-4 with the estimator's answers. Two jobs in the household? Check Step 2(c) on both W-4s.

- Need more withheld fast? Add a flat dollar amount in Step 4(c). It comes out of every check, with no other changes.

- Ask payroll to confirm what's on file. ("Can you check whether an exempt flag is set on my W-4?") Changes apply within 1-2 pay cycles.

- Deep into the year with $0 withheld? Make a direct payment at IRS Direct Pay before December to cut down penalties.

Will I owe? (the safe-harbor rule)

If withholding was too low, the real question is how far off you are. If the shortfall is small, meaning you've paid in at least 90% of what you owe this year, you're fine: no penalty. There's a second escape hatch too. Pay in at least 100% of last year's total tax (110% if your prior-year AGI was over $150,000) and you're protected even if this year's bill is bigger (IRS Topic 306). Miss both and the IRS adds an underpayment penalty on top of the tax.

Example: you'll owe about $3,000 for 2026 and owed $2,500 last year. Get $2,500 in during the year, through withholding or estimated payments, and you can pay the last $500 in April penalty-free.

Special cases

- Teens and first jobs: under $16,100 for the year means $0 withheld is normal, and you likely owe nothing.

- Seasonal or variable hours: withholding swinging check-to-check is the annualizing math, not an error.

- Bonuses: withheld at a flat 22% federal supplemental rate, which is why the bonus check shows withholding even when regular checks show $0.

- Tips and overtime (OBBBA, 2025-2028): you can deduct up to $25,000 in qualified tips and $12,500 in qualified overtime ($25,000 joint) on your return, phasing out above $150,000 MAGI ($300,000 joint). Key point: these happen at filing. They don't stop paycheck withholding. Update your W-4 if you want your checks to reflect them.

Frequently Asked Questions

Is it illegal for my employer not to withhold federal taxes?

Employers must follow your W-4 and the IRS tables. If the tables say $0, that's correct and legal. If they ignored your W-4 or misclassified you to skip payroll taxes, that's a compliance problem. Raise it, and see Form SS-8.

How do I get federal taxes taken out again?

Submit a new W-4: remove an exempt claim, fix Step 3, or add a flat amount in Step 4(c). Applies within 1-2 pay cycles.

Will I owe money at tax time if nothing was withheld?

Only if your income exceeds your deductions. Below $16,100 (single, 2026): no. Above it with nothing withheld: yes. Use the safe-harbor rules to avoid penalties.

Why is Box 2 on my W-2 empty?

Box 2 reports what was actually withheld. $0 there means $0 was withheld all year, for one of the six reasons above.

Does exempt mean I pay no taxes?

No. It only stops income-tax withholding. FICA still comes out, and your wages are still taxable if you're over the thresholds.

Do I still pay Social Security and Medicare if no federal tax is withheld?

Yes: 6.2% + 1.45% on every W-2 check regardless. If those are missing, you're being paid as a contractor.

Sources: IRS Publication 15-T (2026); IRS 2026 inflation adjustments; Form W-4 (2026); IRS Tax Withholding Estimator; IRS Tax Topic 306; IRS Topic 753; IRS OBBBA guidance on tips and overtime. This article is general information, not tax advice. For your specific situation, consult a tax professional.

Kristen Larson is a payroll specialist with over 10 years of experience in the field. She received her Bachelor's degree in Business Administration from the University of Minnesota. Kristen has dedicated her career to helping organizations effectively manage their payroll processes with Real Check Stubs.