Pros and Cons of a Limited Liability Company (LLC)

An LLC protects your personal assets from business debts and lets profits pass through to your personal tax return, which is why most U.S. small businesses pick it.

The downsides are self-employment tax on your profits, yearly state fees you owe even with no income, and a hard time raising money from investors.

The right choice depends on how you'll pay yourself, what state you're in, and whether you need outside funding. Here are the pros and cons to weigh before you file.

What Business Types Should Choose to Become an LLC?

A limited liability company is a U.S. business structure where the owners (called members) are not personally liable for the company's debts. LLCs combine pass-through taxation, like a sole proprietorship or partnership, with the liability protection of a corporation.

An LLC is not a corporation. It is a separate legal entity that gives owners the best of both worlds, which is why it has become the go-to structure for new and small businesses. Rules vary by state, so what works in Delaware may not work the same way in California or Texas.

If you want flexible management, pass-through taxes, and asset protection, and you don't plan to raise venture capital, an LLC is usually the right fit. It suits sole proprietors, partnerships, and small multi-owner businesses that want corporate-style protection without the formalities.

Some businesses can't use the standard LLC structure. Banks and insurance companies are generally barred from operating as LLCs. Licensed professionals like doctors, lawyers, architects, and accountants often have to form a Professional LLC (PLLC) instead, and a few states (notably California) don't allow licensed professionals to use an LLC at all and require a professional corporation.

LLC Requirements

The requirements for forming an LLC may vary from state to state. However, there are still some common grounds across the board, which require you to provide the same information.

- Business Name

The very first thing business owners or company officials must perform is to choose the company's name. The name must be unique and not confusing. Additionally, the name must include the term "LLC" or "Limited Liability Company." Each state has its own unique set of name requirements that you need to know before finalizing the business name.

- Articles of Organization

This is the document you file with the state to officially create your LLC. It lists the basic facts: name, address, registered agent, and members. Filing fees in 2026 range from about $35 (Montana) to $500 (Massachusetts), with most states between $100 and $200.

- Registered Agent

Most states require a registered agent with a physical address in the state of formation. The agent receives legal notices and government mail on the LLC's behalf. You can be your own agent, appoint another member, or hire a service for around $100 to $300 per year.

- Business Licenses and Permits

Creating a company needs a variety of business licenses to operate in your state legally. Depending on the type of business you want to form, these licenses may differ from state to state. You may need to file tax registrations, zoning or land-use permits, health permits, general business licenses, and state-issued occupational licenses, among others. Be careful as filing all these forms in order could become overwhelming.

- Statement of Information Form

Several states (including California, Nevada, and Illinois) require an initial and ongoing Statement of Information that lists your LLC's name, address, members, and managers. California's form is the LLC-12, due within 90 days of formation and every two years after.

- Tax Forms

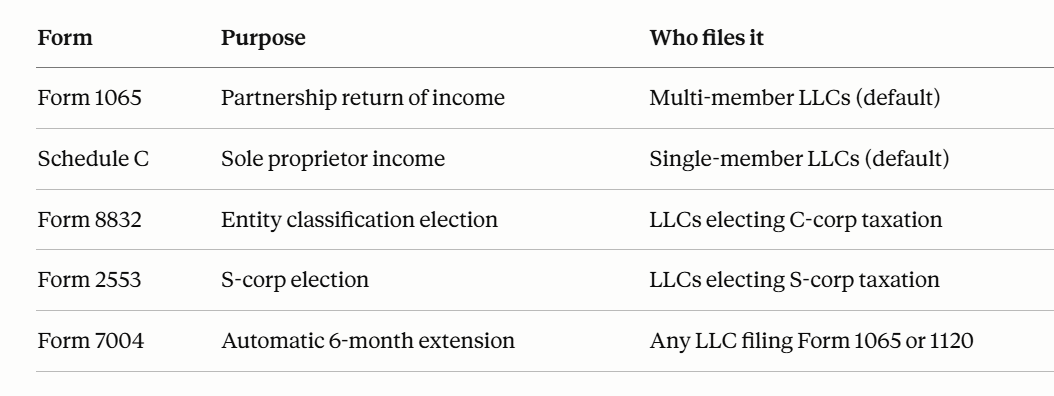

Filed along with other income tax documents, LLC tax form 1065 is the form you would need to use when filing a tax return on partnership income. LLCs and partnerships do not need to pay separate taxes, as they pass through all revenue and losses to the partners.

For the 2025 tax year, calendar-year multi-member LLCs must file Form 1065 by March 16, 2026 (the 15th fell on a Sunday). Form 7004 pushes the deadline to September 15, 2026. The IRS penalty for late Form 1065 filing in 2026 is $245 per partner, per month, for up to 12 months.

Good to Know: IRS Form 2553

- Operating Agreement

Although an Operating Agreement is not a part of the requirements when forming an LLC, it is very significant and highly recommended. This agreement helps create a group where you would not have an upset partner backing out at the last minute or unable to add a new member you want to consider.

The Operating Agreement states several crucial pieces of information, such as investment of additional capital, management structure, division of profits, and the process when a member of the LLC leaves or passes away.

LLC Advantages

- Limited liability

As the name suggests, limited liability is an LLC advantage that protects the owner as well as the shareholders from personal liability from debts and other financial obligations of the business.

- Pass-Through Taxation

LLCs avoid the "double taxation" that hits C corporations. Profits and losses pass through to members and get reported on their personal returns, whether or not cash is actually distributed. The LLC itself usually pays no federal income tax.

- Flexible Management

After filing the Articles of Organization, you have wide latitude to structure how the LLC runs. The operating agreement can customize voting, profit splits, and management roles in ways a corporation can't easily match.

- Hybrid of Corporation and Partnership

An LLC blends features of both. Like a corporation, it's a separate legal entity that shields owners from business debts. Like a partnership, it can be run informally without a board, bylaws, or annual shareholder meetings.

If one member is personally sued or commits an illegal act, the other members and the business itself are generally insulated. Management stays flexible and member-driven, not boardroom-driven.

- Perpetual Existence

Much like a corporation, a limited liability company has perpetual existence, meaning it has a life of its own. It could continue to operate and exist even after the members sell or transfer their shares or die.

- Multiple Tax Options

By default, single-member LLCs are taxed as sole proprietorships and multi-member LLCs as partnerships. You can also elect S-corp or C-corp treatment by filing Form 2553 or Form 8832. The S-corp election often pays off once net profits consistently exceed roughly $60,000 to $80,000, because it can reduce self-employment tax on distributions.

- Fewer Compliance Burdens

In some states, the benefits of an LLC also enjoy fewer compliance issues. This means that the business entity does not need to conduct an annual meeting and less paperwork and recordkeeping compared to a corporation. Additionally, an LLC does not need to have a board of directors.

- Unlimited Number of Owners

LLCs have no cap on the number of members. S corporations are limited to 100 shareholders (and only U.S. individuals or certain trusts), but LLCs can have unlimited members, including foreign owners and corporate members.

- Passive Investors Are Allowed

LLCs can include silent investors who contribute capital but don't manage day-to-day operations, similar to limited partners. The operating agreement should clearly spell out these roles to avoid disputes later.

- Ability to deduct losses

To an extent permitted by law, active members of an LLC can deduct the business's operating losses against the member's regular income. However, this could be seen as a disadvantage to some members who do not want deductions in their income. Owners and shareholders of an S corporation could also deduct operating losses, as opposed to shareholders of a C corporation who cannot.

You may be interested: Top 13 Accounting Advice for Small Business

LLC Disadvantages

Although there are many benefits of an LLC, there are also disadvantages of a limited liability company that you need to consider when forming a business. Here are some of the downsides of opting for an LLC status.

- Harder to Raise Outside Capital

Venture capitalists and most institutional investors won't fund LLCs. They want C corporations, ideally Delaware C corps, because of stock classes, QSBS treatment, and pass-through tax complications. If you plan to raise a serious round, plan to convert.

- State Fees and Franchise Taxes

Many states charge LLCs an annual fee or franchise tax just for existing. California charges every LLC an $800 minimum annual franchise tax (the AB 85 first-year waiver expired at the end of 2023), plus an additional fee if California gross receipts exceed $250,000. Texas, Delaware, New York, and several others have their own annual fees or franchise tax obligations.

- Pass-Through Taxation Can Backfire

Pass-through is usually a feature, but it becomes a drawback when the LLC retains earnings to reinvest. Members owe tax on their share of profits even if no cash is distributed. C-corp owners only pay tax on dividends actually received.

- Less Structure

Unless the business creates a detailed operating agreement and puts it in place, the lack of strict requirements for governing and managing the business could mean problems along the way. Although, making an operating agreement would require the company to pay additional costs for attorney fees.

- Medicare and Social Security Taxes

LLC members generally pay self-employment tax on their share of business income. The 2026 SECA rate is 15.3% (12.4% Social Security on the first $184,500 of net earnings, plus 2.9% Medicare on all earnings, with an additional 0.9% Medicare surtax above $200,000 single / $250,000 married). C-corp shareholders only pay payroll tax on actual wages, not on retained profits.

- Owners Should Recognize Profits Immediately

Shareholders in a C Corporation are not always subjected to tax based on the corporation's profits. This is because a C corporation does not need to immediately hand out its earnings to its shareholders in the form of a dividend. As such, as an LLC avoids double taxation, the company's profits are automatically included in an owner's income.

- Fewer fringe benefits

Fringe benefits refer to benefits that business owners give to their employees that go above and beyond regular financial compensation. They could include group insurance, medical insurance, medical reimbursement plans, and parking.

Unlike employees of a C corporation who do not have to report fringe benefits as taxable income, LLC employees must treat these fringe benefits as taxable income. This is also the case for employees who own more than two percent of an S corporation.

- Dissolution Risk in Some States

A few state statutes still trigger dissolution when a member leaves, unless the operating agreement says otherwise. This is one more reason to have a clear, written operating agreement on file from day one.

Conclusion

An LLC is a strong default for small businesses that want personal liability protection, flexible management, and pass-through taxes. The trade-offs are real (self-employment tax, state fees, and limited fundraising options), but for most independent operators and small partnerships, the benefits outweigh them.

Online formation services can handle the paperwork for $0 to $300 plus state filing fees, but a short call with a CPA or business attorney is worth it before you commit to a tax election.

Once your LLC is up and running, you'll need clean payroll records to pay yourself, your employees, and your contractors. Real Check Stubs is a fast paystub generator that produces accurate, professional stubs in minutes, so you can keep the financial side of your LLC tidy from day one.

Kristen Larson is a payroll specialist with over 10 years of experience in the field. She received her Bachelor's degree in Business Administration from the University of Minnesota. Kristen has dedicated her career to helping organizations effectively manage their payroll processes with Real Check Stubs.

Our all Posts