Payroll Deductions: Definition and Different Types

Payroll deductions are the sum total of funds deducted from the wage of the worker prior to obtaining their net pay. It is the method of deducting different amounts from the gross pay to determine the net pay of the worker. Pre-tax, employee tax withholding, and post-tax are only a few models of the things that qualify as payroll deductions. A percentage of the gross pay of the worker is normally utilized to determine the amount of each payroll deduction. For instance, the number of assistance a worker claims on their W-4 form and their tax bracket is utilized to identify how much federal income tax must be taken out.

What is a Payroll Deduction?

A payroll deduction pertains to the quantity of money that is kept back from the paycheck of a worker by their employer. A payroll deduction is a combination of several purposes, including taxes, insurance policies, retirement savings, charitable donations, or other benefits the employer offers.

It is normally computed as a percentage of the worker's gross income, and they decrease the amount of taxable earnings the worker acquires. The employer is obliged to collect the subtracted amount and remit it to the appropriate government agency or a third-party organization.

Some usual examples of payroll deductions are income tax withholdings, social security and Medicare taxes, health and life insurance premiums, retirement plan contributions, and union dues. The amount of payroll deductions differ based on the earning of the worker, tax status, and the particular benefits and deductions offered by the employer.

How does Payroll Deduction work?

There are numerous ways how payroll deduction works which are seen in every step. Firstly, the employer determines the amount to be deducted by computing the taxes and other benefits from the gross pay. Secondly, the employer obtains the worker’s written authorization prior to the deduction of any amount from the paycheck of the worker. The authorization usually takes the form of a signed paper or electronic agreement.

Thirdly, the employer calculates the payroll deduction again based on the agreed-upon amount or percentage once the necessary authorization has been obtained. Fourthly, the employer deducts the computed amount straight from the paycheck of the worker. Lastly, the deducted funds are remitted to the designated third party, which includes a government agency, insurance organization, or retirement plan administrator.

What is the importance of Payroll Deductions?

The importance of payroll deductions is evident for both the employer and worker benefits. A payroll deduction is highly important in compliance with tax laws as it is required by the law for differing taxes, such as income tax, social security tax, and Medicare tax. Employers must guarantee the exact amount is deducted and remitted on time to avoid fines and legal problems.

A payroll deduction is significant in terms of retirement savings because it aids the workers to save for retirement by contributing to a 401(k) or other retirement plan. These kinds of deductions decrease taxable earnings and supply a convenient way to save for the future. Furthermore, an insurance deduction is part of the payroll deduction which supplies workers with insurance policies, such as health, dental, and life insurance. It aids them to control healthcare expenses and provides financial security when it comes to unexpected events.

Moreover, a charitable contribution is another significance of payroll deductions by which some workers choose to support several causes and organizations through the deductions from their paychecks. Additionally, a payroll deduction aids in budgeting and financial planning by supplying a predictable regular stream of deductions from the paycheck of the worker.

What are the different Types of Payroll Deductions?

The different types of payroll deductions are listed below.

- Pre-Tax Deductions: They refer to the deductions on the salary of the worker before any taxes are removed by the employer. Pre-tax deductions are purposely done to lower the overall liability of the worker in terms of taxes.

- Employee Tax Withholdings: These are the quantity of money that employers take out from the wages of the workers to pay for federal, state, and local income taxes. These are computed from the earnings of the worker, filing status, and the number of allowances they claim on their W-4 form.

- Post-Tax Deductions: These are the forms of deductions that are subtracted from the salary of the worker after taxes have been determined, computed, and deducted. These deductions are often made for payments of debts, voluntary deductions like charitable donations, and union dues.

Pre-Tax Deductions

Pre-tax deductions are amounts that are taken out of the gross pay of an individual prior to taxes computed and withheld by their employer. Pre-tax deductions decrease the taxable earning of a worker, which in turn lowers their overall tax liability. The common examples of pre-tax deductions are contributions to retirement plans which include 401(k)s, flexible spending accounts (FSAs) for healthcare or dependent care expenses, and certain insurance premiums.

There are items like transportation benefits or worker stock purchase plans. Pre-tax deductions have the ability to help workers save money on their taxes while contributing to their long-term financial objectives at the same time by reducing their taxable earnings.

1. Health Insurance Premiums

Health insurance premiums are common payments that are paid by workers to their respective health insurance organizations in exchange for coverage of medical charges. Health insurance premiums are normally paid on a monthly basis, and the money that is utilized to pay differs based on factors including the level of coverage, the age of the worker and health status, and the insurance provider. It is either paid by workers directly, or they are to be paid partially or fully paid by the employers as a portion of a benefits package.

Health insurance premiums are diverse and depend on factors, which include the type of plan, the deductible, co-payments, and out-of-pocket maximums. Higher premiums are associated with plans that supply more comprehensive coverage and lower out-of-pocket costs in general. On the other hand, lower premiums come with higher out-of-pocket expenses.

2. Flexible Spending Accounts

A flexible spending account or FSA is a kind of tax-advantaged savings account supplied by some employers that enable workers to set aside pre-tax dollars to pay for qualified medical or dependent care costs. A flexible spending account (FSA) has contributions that are deducted from the paycheck of the worker prior to the calculation of taxes, which decreases the taxable earning of the worker.

A fundamental component of a flexible spending account (FSA) is that the budgets must be utilized within a particular period of time, normally the calendar year in which they are contributed. However, some plans enable a grace period of up to two and a half months after the end of the plan year or a carryover of approximately $550 in funds that are not utilized into the following plan year. It is a highly important instrument for workers to save money on qualified costs while decreasing their taxable income.

3. Retirement Contributions

A retirement contribution refers to the usual payments by a worker or their employer into a retirement savings account, with the objective of establishing a nest egg for retirement. A retirement contribution has a lot of different components, which include 401(k), individual retirement accounts or IRAs, and pensions. A retirement contribution is a significant way to save for retirement and guarantee a financially supportive future.

A worker is able to make pre-tax contributions from their paycheck directly in a 401(k) plan, which is up to a certain annual limit established by the IRS. Employers sometimes impart to the 401(k) account of the worker, either via a matching contribution or a profit-sharing contribution.

Furthermore, a worker in an individual retirement account (IRA) imparts a certain amount of cash each year. These contributions are made on a pre-tax basis or on an after-tax basis, which highly depends on the form of an individual retirement account (IRA).

Moreover, pensions are retirement plans which an employer imparts for the benefit of a worker to achieve the main objective of supplying guaranteed retirement earnings. Pensions are less usual than they usually do before, mainly because a lot of employers have transferred to 401(k) plans and other defined contributions plans.

4. Transportation Benefits

A transportation benefit is a form of worker benefit that has the ability to help individuals save money on their commute to work. A transportation benefit is typically delivered by employers and comes in several forms, which include pre-tax payroll deductions, employer-paid transit passes, or reimbursements for qualified transportation expenses.

Employers sometimes offer transportation benefits as a before-tax deduction, which suggests the worker has the option to elect to have a cut of their wage set aside and utilize the money to support transportation expenses. For instance, for workers who choose to set aside $1,000 of their salary for transportation expenses, the taxable income becomes $39,000 if they are earning $40,000.

The expenses must be treated as “qualified transportation fringe benefits” under the IRS tax code to become eligible for pre-tax transportation benefits. A typical form of transportation benefit is a commuter benefit program, which enables the workers to utilize pre-tax dollars to pay for eligible transportation costs such as transit passes, parking, and van pooling.

Employee Tax Withholding

An employee tax withholding is a system utilized by authorities to obtain earning tax from the paychecks of the workers. An employee tax is a mandatory procedure in which the employer is demanded to withhold a specific amount of money from the salaries or wages of their workers and transfer it to the authorities on behalf of the workers.

The amount of tax withheld from the paycheck of a worker is identified by the taxable earning, the number of exemptions claimed on the W-4 form and the tax tables given by the government. The taxes that are withheld are then utilized to cover the annual earning tax liability of the worker, which then decreases the amount of taxes that the worker is required to pay in a lump sum at the end of the annual tax.

1. Social Security

Social security is a kind of salary removal that pertains to the cut of the cash that is removed from the wages of the worker by the employer to impart toward future social security benefits. Social Security is a federal government program in the United States that supplies retirement, disability, and survivor benefits to qualified individuals.

Workers and employers are demanded to pay a Social Security tax, which is known as the FICA (Federal Insurance Contributions Act) tax to fund the program. The tax rate is at 6.2% for both workers and employers, which equates to a total of 12.4% in the current era.

The Social Security deduction is normally printed on a pay stub of a worker as a separate line item and is based on the gross earning of the worker. The amount of Social Security taxes that are paid by the worker over the entire span of their job defines the quantity of Social Security benefits they are qualified to acquire in the future.

2. Medicare

Medicare pertains to the national health insurance scheme in the United States that renders coverage and policies for respective healthcare services to individuals aged 65 and above. Medicare is allowed to be utilized for particular impairments or chronic illnesses aside from elderly people.

The program is allocated by the Centers for Medicare and Medicaid Services or CMS and is being funded via payroll taxes, premiums, and general revenue. It has four parts which are Part A for hospital insurance, Part B for medical insurance, Part C for medicare advantage, and Part D for prescription drug coverage. Medicare is an overall essential healthcare coverage that provides benefits to millions of Americans and aids to guarantee that the elderly and those people with impairments have adequate admission to demand medical assistance.

3. Federal Income Tax

Federal income tax is a tax on the wage of a worker charged by the federal authority. Federal income tax is considered progressive, which indicates that the tax rate is gradually elevating as the taxable earning of the worker is increasing.

The main objective of the federal income tax is to raise gains for the federal government to allocate a budget for its processes and programs, which include national security, social security, Medicare, and establishments. The federal income tax is accumulated and acquired by the Internal Revenue Service or IRS and is founded entirely on the taxable earning of the worker, which is computed by subtracting allowable deductions from the total earning.

4. State Income Tax

State income tax pertains to the deductible that is levied on the earnings acquired by individuals, organizations, and other establishments within a specific state. State income tax is accumulated and obtained by the state authority. The revenue earned from the tax is utilized to allocate a budget for several public assistance and schemes, including education, health care, transportation, and public safety and security.

The quantity of state income tax that a worker or organization is required to pay is normally based on the taxable earning, which is computed by deducting any permissible deductions from their total income. The tax rate differs based on the state, with some states possessing a flat tax rate, while others are implementing a progressive tax rate.

Post-Tax Deduction

Post-tax deductions are the collection of diverse components of expenses or contributions that are deducted from the earnings of a worker after taxes have been computed and withheld. Post-tax deductions are taken out from the paycheck of a worker after the income taxes have been deducted and mostly include things like retirement contributions, health insurance policies, and charitable donations. One of the most common examples of a post-tax deduction is Roth 401(k).

Post-tax deductions are not referred to with similar conditions and limitations as pre-tax deductions, and the quantity a worker is able to impart is typically unlimited. However, these deductions do not supply the same tax advantages as pre-tax deductions, mainly because they are claimed after taxes have been taken out from the salary.

1. Child Support

Child support is a form of post-tax deduction that pertains to the quantity of money that a noncustodial parent pays to a custodial parent. Child support serves as assistance for their child after taxes have been withheld from the earnings of the noncustodial parent.

Child support payments in the United States are typically not tax-deductible for the paying parent, and they are not treated as taxable earnings for the receiving parent. Hence, the post-tax quantity of child support refers to the amount of money that is actually obtained by the custodial parent from the noncustodial parent after tax deductions. The specific rules and regulations regarding child support vary by state and country, which means there are different rates and ways of deductions.

2. Charitable Donations

Charitable donations post-tax are the act of allocating money or assets to an eligible charitable institution after taxes have been paid on the earnings utilized to create the donation. Charitable donations are capable of reducing the overall tax liability from the taxable earnings.

For instance, the tax liability has the possibility to be decreased by $500 if a worker donates $2000 to an eligible charity and is in a 25% tax bracket, assuming that the worker itemizes the deductions on the tax return. However, the worker is not able to claim the charitable donation as a deduction if the standard deduction has been chosen and taken.

There are charitable donations that are tax-deductible, but there are others that are not. The company must be a qualified nonprofit organization recognized by the IRS. Furthermore, there are limitations to how the amount of deduction based on the income of the worker or organization and the form of a donation to make.

3. Wage Garnishments

Wage garnishments are legal procedures in which a cut of the earnings of a worker is deducted by the employer to pay a debt that is owed to a specific creditor. The quantity of how much the allowable deduction from the wages of the workers are generally identified by state and federal laws, and established on elements such as the form of debt, the amount of debt, and the worker’s earning.

Wage garnishments are commonly formed by a court order or an authoritative agency, which includes the Internal Revenue Service (IRS) or the Department of Education. The employer of the worker is legally required to subtract the stipulated amount from the paycheck and send it to the creditor or agency directly once the demand has been imposed.

They have a crucial influence on the finances of a worker, mainly because they have the capacity to reduce disposable earnings and make it harder to compensate for essential living expenses. Wage garnishments are the sole choice for creditors in some cases to obtain the owed money that has never been paid.

4. Roth 401(k) Contributions

A Roth 401(k) contribution is one of the several types of retirement savings programs that enable workers to impart after-tax money to their retirement account. A Roth 401(k) contribution is made with money that has already been subtracted by taxes; hence, there are no taxes on withdrawals upon retirement of the worker.

The contribution limit for a Roth 401(k) is approximately $19,500 in 2021 and has an extra catch-up contribution of $6,500 for those who are 50 years old or older. Employer contributions to a Roth 401(k) are done with before-tax money, so they are subjected to taxes when withdrawn during retirement.

An advantage of a Roth 401(k) is that it supplies diversification of tax during retirement. Withdrawals are taxed as ordinary earnings with a traditional 401(k). However, withdrawals are free from taxes with Roth 401(k), which is highly beneficial if tax rates are higher in the future.

How do different Types of Payroll Deductions affect employees' wages?

The different types of payroll deductions affect employees’ wages by making them lesser as more deductions are being taken out. A worker is highly impacted by the deductions in terms of financial security because sometimes the deductions are too much that they make someone incapable of sustaining their daily needs. For instance, a $500 salary with $250 deductions from both pre-tax and post-tax are most likely to cause drastic effects on one’s way of living.

However, there are types of payroll deductions that do not have extreme effects on the wages of the workers. There are workers that do not have any ongoing debts and do not engage in voluntary payroll deductions which makes them more financially advantageous. The higher the payroll deductions, the more deranged the wages of the employees. Therefore, workers must avoid having debts and secure more money on their insurance, medicare, and social security, among others.

How can employees verify different Types of Payroll Deductions?

There are various ways on how employees are able to verify different types of payroll deductions. Firstly, review the pay stub after receiving it together with a paycheck which are two documents that show details of the earnings, deductions, and net pay. The pay stub must always include a breakdown of all payroll deductions.

Secondly, a worker must check the W-2 form which is obtained at the end of the year from the employer. Its purpose is to summarize the earnings and deductions of the year. The W-2 form must possess detailed information on all the payroll deductions for the entire year.

Thirdly, the worker must contact the employer or payroll department if there are queries about the payroll deductions to obtain clarification. Employers and payroll agencies are accountable for guaranteeing that payroll deductions are precise and abide by all the applicable laws and regulations; hence, they must be able to supply workers with accurate details.

Lastly, the workers must recheck the benefits enrollment information if they have any voluntary deductions for certain types of benefits. They have permission to review their benefits enrollment information to verify the amount of their deductions and the benefits they are currently obtaining.

Can employees verify different Types of Payroll Deductions through a Paycheck?

Yes, employees can verify different types of payroll deductions through a paycheck. A paycheck is designed to provide a concise version of all the payroll deductions that are deducted from the gross pay of the worker. A worker is allowed to review the paycheck to confirm that the exact amounts have been taken out from the paycheck for each payroll deduction.

Furthermore, workers must verify the overall net pay on their paycheck is correct aside from the amounts taken out for each deduction. The worker must bring the concerns to the employer or payroll agency as early as possible if there are discrepancies noticed in the net pay or in the amounts that are deducted.

How to Calculate Payroll Deductions?

The steps to calculate payroll deductions are listed below.

- Determine the gross pay: It refers to the step of identifying the total amount of pay a worker gains before any taxes or deductions are taken out. It is the full salary of the worker that is supposed to be acquired if there are no deductions.

- Identify the payroll deductions: It determines which payroll deductions are applicable to the worker, and mostly they are the federal income tax, social security tax, and Medicare tax. Additionally, it includes voluntary deductions such as retirement contributions, health insurance premiums, or wage garnishments.

- Determine the amount of each deduction: It is the phase by which the employer computes the amount to be subtracted from the gross pay of the worker for each payroll deduction. There are deductions that are fixed amounts, while others are a percentage of the gross pay of the worker.

- Remove the deductions from the gross pay: Remove the complete amount of deductions from the gross pay to identify the total value of the net pay of the worker, which is the amount to be acquired in the paycheck.

- Verify accuracy: The calculations must be checked twice by the employer to guarantee that the correct quantities are being subtracted and the net pay is entirely precise. It is done to avoid errors that result in legal disputes.

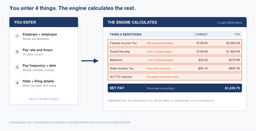

Does a Payroll Deductions Calculator be used in calculating Payroll Deductions?

Yes, a payroll deductions calculator is used in calculating payroll deductions. A payroll deductions calculator is an instrument that aids to identify the exact amounts to be withheld from the salary of a worker for taxes and other payroll deductions. These calculators are able to be accessed on the internet, and a lot of payroll software applications include a calculator feature.

An employer is required to encode details such as the gross pay of the employee, federal tax withholding status, state tax withholding status, and any other extra payroll deductions to use a payroll deductions calculator. The calculator then supplies the employer with the highly accurate amount to be subtracted for each deduction along with the net pay of the worker once the complete details are encoded.

The usage of a payroll deductions calculator is highly important since it conveniently aids the employer to guarantee that payroll deductions are computed precisely and effectively. Furthermore, it aids employers and workers to better comprehend the influence of taxes and other forms of deductions on the salary of the worker.

How are Payroll Deductions reflected on an employee's Paycheck?

Payroll deductions are reflected on an employee’s paycheck as a reduction in their gross pay, which is the before-tax salary. These removals and their full quantity for each payment course are deducted from the gross pay to identify the net pay of the worker. A typical paycheck shows and lists the payroll deductions in a different area from the gross and net pay amounts. Every single payroll deduction that is being taken out by the employer is reflected on the paycheck to ensure pure transparency between the two groups. The usual payroll deductions that are printed on the paycheck of a worker are federal income tax, state and local taxes, Social Security tax, and Medicare tax, among others.

Do these Payroll Deductions appear in Payroll?

Yes, payroll deductions appear in Payroll. Payroll deductions are already included in the payroll which is highly specified to let the worker know how these deductions are made and calculated.

The payroll deductions are often recorded under a different portion of the payroll and have the name of the deduction, the amount that has been subtracted, and the meaning of the deduction. For instance, the payroll lists the amount deducted for life insurance and the name of the organization if the worker has a payroll deduction for life insurance. Payroll deductions must always appear in payroll to provide a clear understanding of the deductions from gross pay to net pay, which makes complaints and issues preventable.

Does Payroll Deductions appear in Paystub?

Yes, payroll deductions appear in pay stubs. A pay stub is a paper or electronic documentation that is released together with a paycheck and supplies detailed data regarding the earnings of a worker and deductions for a given pay period. Payroll deductions are listed in every paystub that is distributed along with their amounts, so workers are able to see completely how much was subtracted from their gross pay to arrive at their net pay.

A pay stub is highly informative when it comes to displaying the deductions since every single dollar is recorded on the detailed breakdown. It is very important for transparency and mutual understanding between the employer and the worker.

What is the difference between Voluntary and Involuntary Deductions?

The difference between voluntary and involuntary is seen in the process of taking out the deduction. Voluntary deductions refer to the deductions that the worker picks out of their salary. Voluntary deductions are normally created for benefits which include health insurance, retirement savings plans, or flexible spending accounts.

On the other hand, involuntary deductions are money that is subtracted required by law or as a consequence of a court order. These kinds of deductions mostly include taxes such as social security, Medicare, and federal and state earning taxes. Additionally, these include wage garnishments for stuff like child support, unpaid taxes, and other forms of debt.

Voluntary deductions are optional and are frequently done at the permission of the worker, while involuntary deductions are obligated and are not allowed to be refused by the worker. Employers are obliged by law to facilitate these deductions from the salary of the worker, and penalties or legal actions are expected if there are failures to initiate these deductions.

Kristen Larson is a payroll specialist with over 10 years of experience in the field. She received her Bachelor's degree in Business Administration from the University of Minnesota. Kristen has dedicated her career to helping organizations effectively manage their payroll processes with Real Check Stubs.

Our all Posts